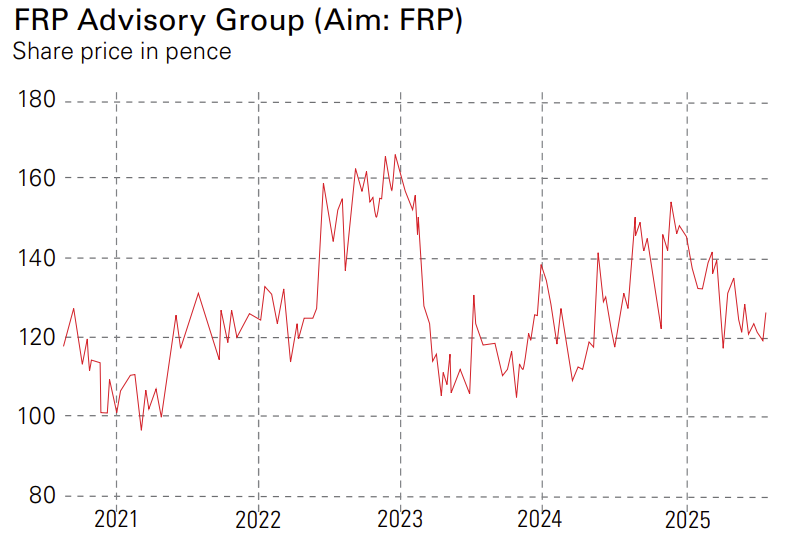

FRP Advisory Group (Aim: FRP) is a leading advisory company specialising in restructuring and insolvency services across the UK, with a market share of 12%. Over the past decade, it has expanded and doubled down on its position, increasing its share of the market threefold from 4% at the beginning of the 2010s. The firm has grown despite a relatively benign backdrop for insolvencies and restructurings. According to the Insolvency Service, the number of corporate insolvencies reached a high of 24,000 in 2009 (across England and Wales) before declining to 14,500 a year in 2015, 2016 and 2017, before rising slightly to 17,000 in 2019 and then falling again to a multi-decade low of 12,300 in 2020.

In the years between 2009 and 2019, struggling businesses were supported by low interest rates and modest economic growth, but all that changed in 2022. Government-backed schemes to support businesses helped stave off a complete collapse in activity during the pandemic. But as the schemes were withdrawn and interest rates rose, the number of firms falling into distress also climbed. From a low of 12,631, the number of insolvencies in England and Wales more than doubled to 25,164 in 2023.

FRP Advisory Group’s expansion plans

FRP entered this environment in a position of strength. The company floated on the Aim junior market in March 2020, raising £20 million by placing new shares to boost its balance sheet and fund acquisitions. Since then, it has splurged on deals, with 14 completed from the time of the IPO to May 2025 and five deals completed in its 2025 financial year alone.

Subscribe to MoneyWeek

Subscribe to MoneyWeek today and get your first six magazine issues absolutely FREE

Get 6 issues free

Sign up to Money Morning

Don’t miss the latest investment and personal finances news, market analysis, plus money-saving tips with our free twice-daily newsletter

Don’t miss the latest investment and personal finances news, market analysis, plus money-saving tips with our free twice-daily newsletter

These deals have helped FRP expand beyond its traditional markets. For example, in May, it acquired One Advisory Group, which provides financial reporting and transaction advice, and governance services to more than 100 clients, the majority of which are listed on the London Stock Exchange. All these deals were funded with the company’s plentiful cash resources. Net cash was £33 million at the end of fiscal 2025, a little under 10% of the company’s market capitalisation.

According to Berenberg, which has analysed the company’s M&A-driven revenue expansion, these deals accounted for around half of revenue growth (20.5%) in 2022. Still, in fiscal 2023 and 2024, M&A growth was almost entirely non-existent compared with organic growth of 9.3% and 23.3% respectively. In fiscal 2025, deals accounted for about 40% of the company’s 18.7% top-line revenue growth.

Deals have been core to the company’s growth proposition, but so has the operating environment. Revenue has grown at a compound annual growth rate of 15% over the past decade, says Berenberg, as the number of corporate insolvencies rose significantly. The trend is continuing. The latest figures from the Insolvency Service suggest the number of registered company insolvencies in England and Wales rose 8% month-on-month in May 2025 and 15% year-on-year. Monthly insolvency numbers in the first five months of 2025 were higher than in 2024 and at a similar level to 2023, which saw a 30-year high in the annual number of insolvencies.

(Image credit: Future)

FRP Advisory Group’s corporate finance arm

FRP has diversified from its core business of restructuring (although that still accounts for 70% to 80% of group revenue). Not all businesses that run into difficulties end up collapsing. Some are acquired, and some manage to agree a deal with creditors. Even here, FRP’s corporate finance business (15% to 20% of revenue) has a strong foothold in the market. It was the 19th-most-active M&A adviser in the year, being involved in 76 successful deals, averaging £20 million in deal value. This suggests FRP is firmly established in that mid-market bracket of firms that form the backbone of the UK economy.

Berenberg has pencilled in pre-deal revenue growth of 7.7% in 2026, 4% in 2027 and 4% in 2028. Earnings are expected to grow at a much faster clip. Thanks to its successful integrations, the company has sector-leading margins, with a 27% earnings before interest, tax, depreciation and amortisation (Ebitda) margin, exceeding its peer group average of 24%. As such, analysts have pencilled in Ebitda growth of 8.9% in 2026 on a margin of 27.5%. Return on capital employed (Roce), a measure of profit for every pound invested, is expected to be 34.9% on a forward basis.

Undervalued growth

These are all very impressive figures, but despite FRP’s growth, profitability and strong balance sheet, the market doesn’t seem to be interested. The stock is trading at a forward price/earnings (p/e) ratio of just 10.2, falling to 9.8 based on 2027 estimates. It also offers a forward dividend yield of 4.6%. Strip out cash, which is expected to hit £39 million at the end of 2026 (assuming the firm does not find any further deals), and the p/e falls to around nine times on a forward basis.

Based on these numbers and compared to the peer group average, Berenberg believes the stock is deeply undervalued. They’ve pencilled in a price target of 220p per share, suggesting a potential upside of around 72% from current levels, excluding the dividend yield on offer. Some caution is warranted, as restructuring is an inherently cyclical business. If interest rates fall and the government decides to take more action to stimulate business in the UK, the number of restructuring and insolvency deals will almost certainly fall. Still, FRP’s management team has demonstrated over the past five years that the company has what it takes to manage the cycle and even grow during tough periods.

This article was first published in MoneyWeek’s magazine. Enjoy exclusive early access to news, opinion and analysis from our team of financial experts with a MoneyWeek subscription.