When I began contributing to MoneyWeek two decades ago, Britain was in the middle of a property mania. Flipping houses was the path to rapid riches. TV shows were full of people renovating flats to sell – often spending more than they earned back. Financial-advice columns were stuffed with those who wanted to gear up their buy-to-let portfolio to buy more, or had already borrowed too much and were panicking.

Today, Britain is still obsessed with property, but the mood is very different. It’s not simply that investing in property is less appealing due to tax changes and new laws. There has finally been some long-overdue realisation that expensive housing is a curse that holds back the economy, not a source of good fortune.

Still, I am not as confident as Matthew Lynn that property prices are going to plummet to reasonable valuations. Houses are not like most assets: many people buy once they can afford to because they are tired of renting sub-standard properties or because they want to be certain of housing costs for later in life – even if they think prices are expensive. Unless interest rates soar (which seems unlikely) or supply vastly increases – and the government doesn’t have the appetite to provide the state backing needed – a crash is less probable than a long stagnation.

Subscribe to MoneyWeek

Subscribe to MoneyWeek today and get your first six magazine issues absolutely FREE

Get 6 issues free

Sign up to Money Morning

Don’t miss the latest investment and personal finances news, market analysis, plus money-saving tips with our free twice-daily newsletter

Don’t miss the latest investment and personal finances news, market analysis, plus money-saving tips with our free twice-daily newsletter

Housing market stagnation

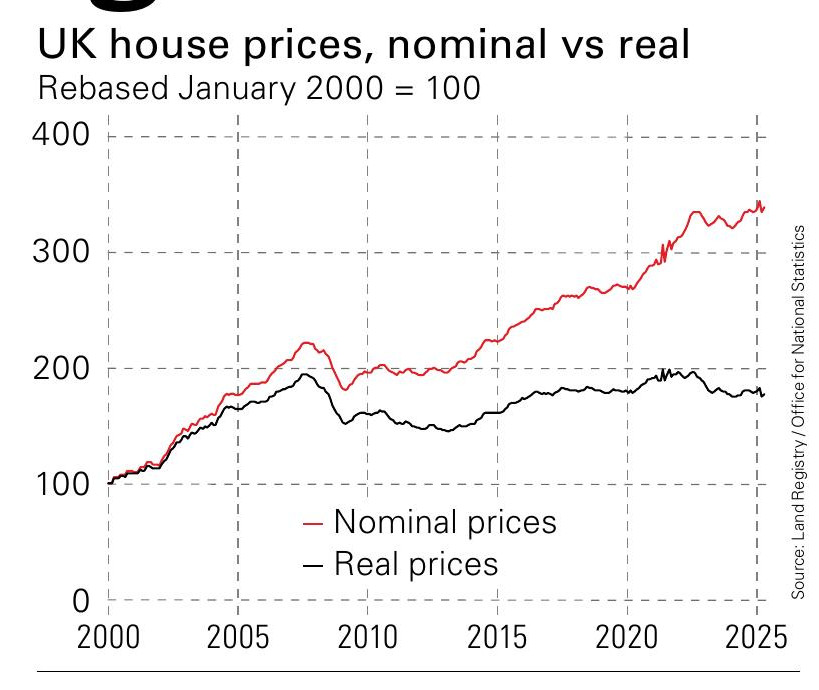

In fact, quiet stagnation is what we have been seeing for a while. For this, refer to the Land Registry data: it is much less timely than other indices (sales can take a very long time to be added) and so doesn’t show turning points well, but it provides the most comprehensive view of long-term trends.

(Image credit: Land Registry / ONS)

(Image credit: Land Registry / ONS)

These series show that house prices have risen strongly in nominal terms since the global financial crisis. Yet adjust for inflation and it’s a different story – real house prices are now below where they were in 2007. Of course, housing is not one market; property type and location are critical. Look at London and we see stagnation since 2016 but also a gulf opening up between terraced houses and flats. Still, even flats are only back to 2007 levels in real terms, when they were already unprecedentedly expensive relative to incomes. Britain’s financial centre has a stagnant yet still-overpriced housing market and a shrinking yet arguably undervalued stock market. No wonder the mood is so bleak.

This article was first published in MoneyWeek’s magazine. Enjoy exclusive early access to news, opinion and analysis from our team of financial experts with a MoneyWeek subscription.