Investors in 2025 are either anxious or happy. The anxious believe investing is all about costs. Buy some cheap trackers, and in the long run, you’ll do fine with minimal effort. The happy are active investors who have avoided the largest stocks. It is an anomaly for the largest stocks to lead the market (1929, 1972, 1999 excepted), and following the crowd into richly valued areas doesn’t end well.

As an active manager, I have found 2025 rewarding mainly because my portfolios pursued value outside the US. A weak dollar has meant US equities have lagged the world. US equities have delivered zero returns in sterling this year, and the MSCI World index, with 70.3% exposure to the US, is up just 2.4% including dividends. Contrast that with the FTSE 100, up 12%, or the pan-European EuroSTOXX, up 20% this year. US exceptionalism has once again been exaggerated.

Passive investing makes sense for people who do not want to take an interest in their finances, which presumably counts out MoneyWeek readers. It delivers a market return, before fees, and prevents a worse outcome from incompetent active managers or bad actors. Being cheap and simple, it deserves to be the default option for the majority, and rightly so. After all, beating the markets is a minority sport.

Subscribe to MoneyWeek

Subscribe to MoneyWeek today and get your first six magazine issues absolutely FREE

Get 6 issues free

Sign up to Money Morning

Don’t miss the latest investment and personal finances news, market analysis, plus money-saving tips with our free twice-daily newsletter

Don’t miss the latest investment and personal finances news, market analysis, plus money-saving tips with our free twice-daily newsletter

Therein lies the opportunity. Passive management is now so vast that, according to US investment platform Market Structure Edge, trading in index products accounts for 56% of market volume; in 1995, it was in its infancy. If passive management today is so vast, it means active management should provide fertile grounds for rich pickings.

This is reaffirmed by a recent market trend that shows active fund-management companies on the up this year, while the passive managers are waning. For example, shares in institutional active manager Schroders are up 25%, while BlackRock, owner of iShares, is down for the year. Is this a one-off? I don’t think so, because the valuation gap is enormous. Schroders trades on twice sales, with a free cash-flow yield of 16%. Contrast that with BlackRock on a hefty eight times sales with a free cash-flow yield below 3%.

Youthful investors forget, or have never witnessed, that active managers were among the most highly rated stocks in the 1990s. Today, they are dirt cheap. My recent picks include Man Group, Jupiter, and the Dutch company Allfunds, which provides trading infrastructure for the funds sector.

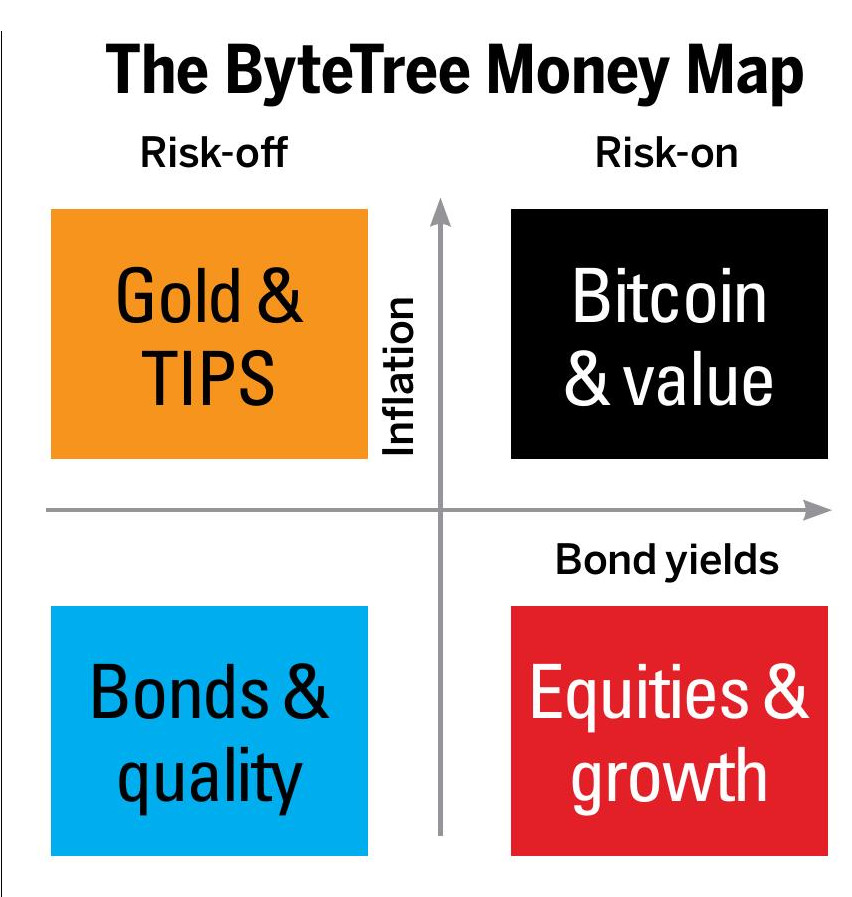

The investors’ Money Map

Other investment themes that stand out include gold, precious metals and copper – all beneficiaries of a weak dollar, money printing, and burgeoning deficits. There’s bitcoin and crypto, which are increasingly looking like core allocations. There are also the banks, which benefit from high interest rates, and China, which has impressive technology companies trading on attractive valuations.

On the other hand, 2025 has been another year to avoid gilts. The long bond yield has settled at 5.5%, a level not seen since 1998. It is supposed to mimic annual nominal GDP growth, which comprises economic growth (1.3%) and inflation (4.4%), so the yield is about right. For it to come down, we would need to see a recession to break inflation, tough love in dealing with the budget deficit, or “growth” policies that don’t involve raising taxes. A recession will come about sooner or later, as they always do, but a balanced budget? Unlikely.

The economy may be in better or worse shape next year, but does it matter? In 30 years since I took an interest in financial markets, I am certain that value is more important than the economy. Therein lies the importance of my Money Map (pictured), which I last wrote about for MoneyWeek in 2017: What to take with you in the investment jungle. It outlines the investment strategy most suited to different macroeconomic environments. When times are good, stay on the right, and when bad, stay on the left. When inflation rises, stay high, when it is low and stable, duck.

(Image credit: Charlie Morris)

I have long built portfolios around this idea, filled with undervalued stocks, bonds, commodities, or funds. The Money Map helps to identify the key areas on which to focus, and more importantly, the areas to avoid. Above all, this is how to diversify a portfolio: by having exposure to each quadrant, whatever the weather, because macroeconomic environments can change quickly.

That said, I have more exposure to the favoured quadrant, and to the adjacent quadrants, with less in the least-favoured one. In recent times, this has meant having more value, and less quality and bonds in the portfolios, while staying broadly neutral in growth and gold. At some stage, this will change, probably when there are clear signs that inflation is under control and interest rates fall.

I am looking forward to that because you will have noticed that quality stocks such as Unilever, Diageo, and Reckitt Benckiser have struggled in recent years and now offer good value. In the US, quality stocks such as Nike, Procter & Gamble, McDonald’s and PepsiCo are also waning, and maybe they’ll be cheap by 2026, or 2027. In any event, the world’s best companies have had their bubble pricked and are headed lower, which is something to look forward to.

Charlie Morris is the CEO and founder of ByteTree. It offers investment research for private clients through the Multi-Asset Investor, in addition to other research services. ByteTree also has a Bitcoin and Gold ETF (BOLD) managed by 21Shares in Zurich.

This article was first published in MoneyWeek’s magazine. Enjoy exclusive early access to news, opinion and analysis from our team of financial experts with a MoneyWeek subscription.